The recent back-to-back repo rate hikes by RBI have increased the EMI burden of home loan borrowers. In this article, we will see how this increase in interest rates has affected home loan EMIs and what could be a solution for home loan borrowers.

The Repo rate maintained by RBI acts as a benchmark interest rate basis on which banks in India offer loans and accept deposits.

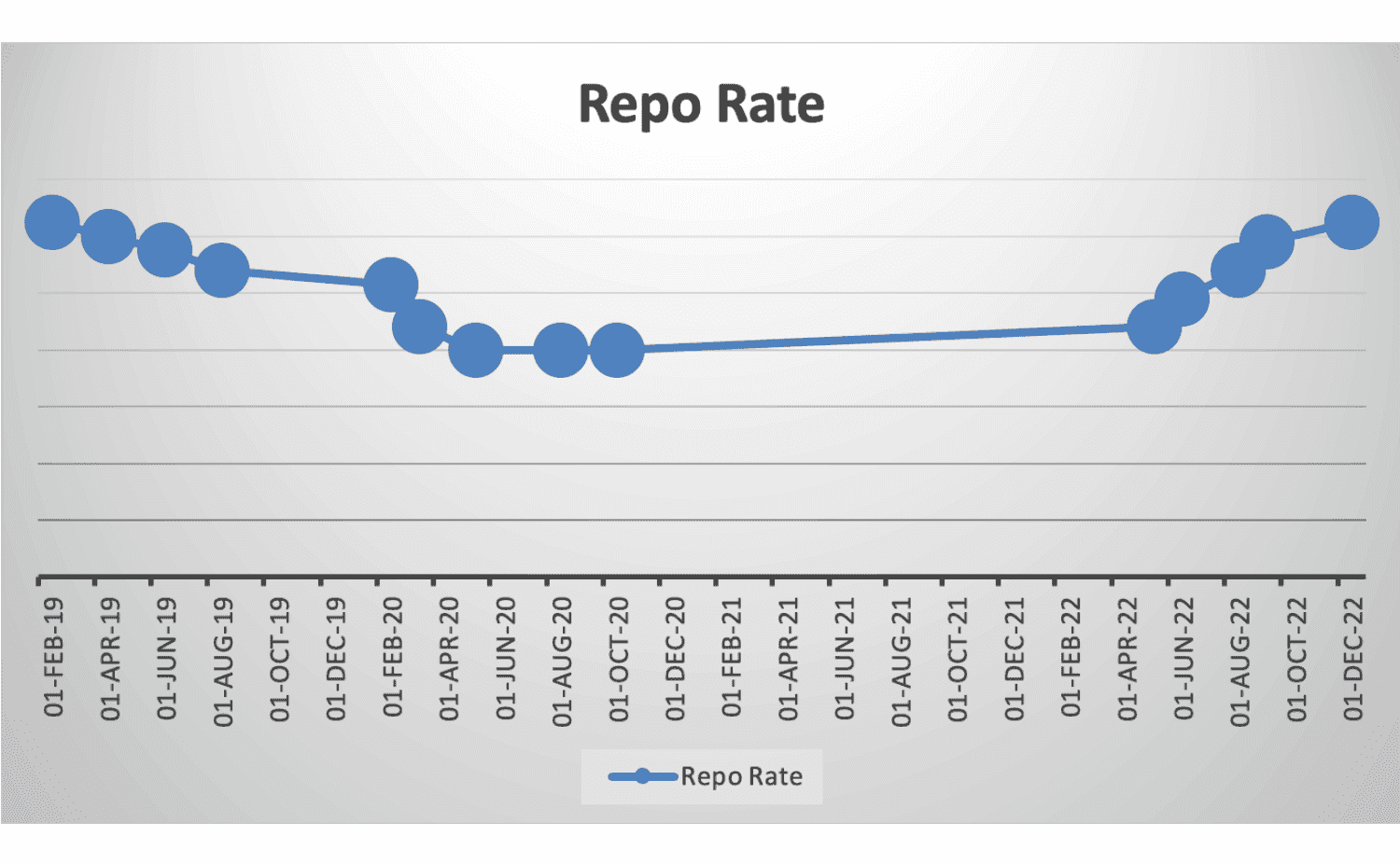

In 2019, the repo rate was 5.40%, and we all know that as we entered 2020, the pandemic gripped us and impacted economic growth globally. To avoid a large-scale closure of business units and maintain liquidity in the banking system, RBI reduced the repo rate to 4% in three meetings.

As a result of this, the home loan interest rate too got revised to an all-time low i.e., in the range of 6.50% – 6.75%, and the real estate market recorded record deals during this pandemic period.

Now we are in 3rd year from the start of this pandemic, cases have reduced globally, most of the economies have opened and now we are facing a hyperinflationary situation caused partly by higher demand on account of the reopening of economies and partly because of supply-side problems due to heightened geopolitical escalations.

This has caused the repo rates and interest rates across the globe reaching to a multi-year high. The situation is still under control in India, but some of the developed countries are facing interest rates at a multi-decadal high.

So, let’s evaluate the impact on home loan EMIs.

Let’s assume that you had taken a home loan of Rs. 1 crore at a 6.75% interest rate last year for a 20-year period. Your EMI would have been Rs. 76000 approximately until May 2022. Since, then in every two months, your EMI would have revised upward on account of interest rate revisions. At present, you would be servicing your home loan at 8.50% – 9% p.a. Which means your EMI has been increased by more than Rs. 10,000 a month. Rs. 10,000 may look small amount, but at this interest rate, you will end up paying approx. 25 lakhs more to your loan provider in your course of loan repayments.

There is a fair bit of chance that interest rates will increase more and thus your loan EMIs are likely to increase further. And by any chance, if you are not in a situation to afford this increase in EMI, and opt for an increase in tenure of your home loan, you will end up repaying your home loan for additional 11 – 17 years from the initial repayment period. That means you will end up paying an extra 1 crore to 2.5 crore.

So, What Is The Way Out?

Shift to an overdraft-based home loan. Let’s see how that will be helpful.

Here, your loan provider will also open an overdraft account for you. There you can park your idle funds and if required you can withdraw that too. Thus, you maintain liquidity for your financial emergencies. And for this liquidity, the interest rate on this type of home loan is a little higher. I have assumed a 0.25% higher interest rate in this illustration.

Let’s assume that from last year, you have been able to save some amount from your income or you have a corpus maintained in a liquid fund or bank fixed deposit for your financial emergencies, or some amount lying idle in your savings or current account due to your business needs. We need to place this amount into the overdraft account. Whatever amount will be kept in this overdraft account, will get adjusted against the home loan principal amount and a relatively larger part of your EMIs will go towards the repayment of the principal. In this illustration, you can see that if this borrower maintains approx. 17 – 20 lakhs in the overdraft account, he can avoid additional repayments in the form of higher EMIs or longer loan tenure. Even if, he is not having enough savings to avoid the complete impact of an interest rate rise, he can reduce the impact by maintaining a smaller amount in the overdraft account.

And let’s suppose, interest rates again start falling, then they will be able to repay their home loans faster. This is happening because whatever amount is maintained in the overdraft account, gets fully adjusted from the outstanding loan amount. Therefore, a relatively bigger part of their EMIs goes towards payment of the principal loan amount. You would notice here that in future if interest rates fall to 7% and 6%, your loan will get finished in around 13 years only resulting in savings of approx. 38 – 48 lakhs.

We focus on Innovation and excellence in Personal Finance. We guide our clients in managing their finances and in meeting their life goals. Please write to us at support@millionsworth.com.