The Big Picture: Divergence in the Global Economic Landscape

This week, the Global Economic Landscape presented a story of sharp contrast and shifting tides. While major Western economies wrestle with sticky inflation and uncertain growth, India has taken a decisive step toward monetary easing. Meanwhile, in a surprising twist, Japan appears poised to move in the opposite direction, signaling a potential tightening of policy.

The defining theme for the week ending December 6, 2025, is Policy Divergence. The Reserve Bank of India (RBI) unanimously voted to cut interest rates to fuel growth. Conversely, reports from Tokyo suggest the Bank of Japan is preparing to raise rates, marking a significant departure from its historical stance. For investors navigating this shifting Global Economic Landscape, understanding these opposing currents—easing in India versus tightening in Japan and stubborn inflation in the US—is essential for effective decision-making.

Here is a detailed look at the data driving these trends.

🇮🇳 The India Story: A Pivot Toward Growth

While uncertainty characterizes much of the Global Economic Landscape, India delivered clear signals of structural resilience and policy support this week.

RBI Cuts Rates: The Monetary Policy Committee (MPC) reduced the repo rate by 25 basis points to 5.25%. This move is aimed at stimulating growth, supported by a benign inflation outlook (projected at 2.0% for fiscal 2026).

GDP Outlook Strengthens: The RBI projects real GDP growth for fiscal 2026 at 7.3%. Echoing this sentiment, Fitch Ratings upgraded India’s growth forecast to 7.4%, citing robust domestic demand and improved consumer sentiment following GST reforms.

Liquidity Measures: To ensure these rate cuts effectively reach borrowers, the RBI announced ₹1,00,000 crore of Open Market Operation (OMO) purchases and a $5 billion Buy-Sell swap.

Government Focus: Strategic initiatives continue to bolster the economy. PM Narendra Modi highlighted potential in India-Russia trade, targeting $100 billion. Meanwhile, the Andhra Pradesh government allocated land for a major 1 GW AI Data Centre, reinforcing the infrastructure push.

🌏 Update on the Global Economic Landscape

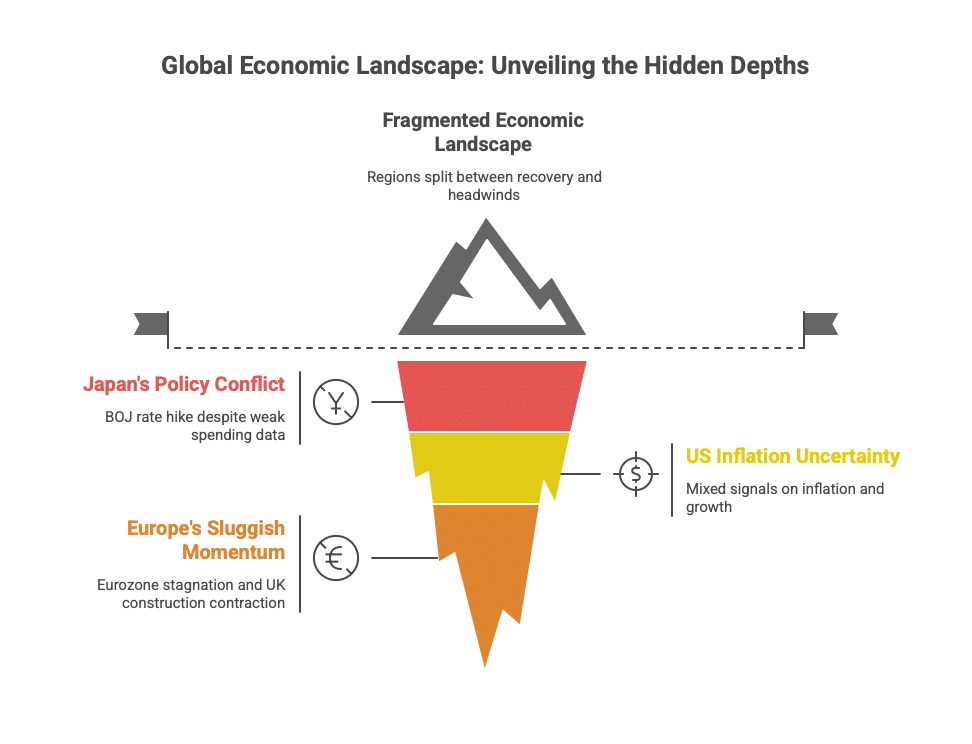

Beyond India, the data points paint a fragmented picture. The Global Economic Landscape is currently split between regions showing recovery and those facing renewed headwinds.

🇯🇵 Japan: A Critical Policy Shift? Japan provided perhaps the most complex signal this week.

- The Data: Household spending fell 3.0% year-on-year in October, reversing previous gains and indicating that consumer caution remains high.

- The News (BOJ Hike): Despite this weak consumption data, reports indicate the Bank of Japan (BOJ) is likely to raise interest rates in December, a move the government is reportedly willing to tolerate.

- Interpretation: This represents a significant conflict in the Global Economic Landscape. While the data (weak spending) suggests a need for support, the central bank appears focused on normalizing policy and defending the currency. A December rate hike would strengthen the Yen but could dampen domestic consumption further. This creates a “tightening” dynamic in Asia just as India enters an “easing” cycle.

🇪🇺 Europe & 🇬🇧 UK: Sluggish Momentum Europe remains a weak link in the current Global Economic Landscape.

- Eurozone Stagnation: The Eurozone economy grew by just 1.4% year-on-year in Q3, signaling a continued slowdown.

- UK Housing vs. Construction: While the UK Halifax House Price Index rose 0.7%, the construction sector is contracting sharply, with the S&P Global Construction PMI falling to 39.4.

🇺🇸 United States: Mixed Signals on Inflation The US economy continues to send conflicting signals.

- Inflation Ticks Up: US annual PCE inflation accelerated to 2.8% in September, up from 2.7% previously.

- Growth Persists: Industrial production increased by 1.6%, suggesting economic activity remains resilient. However, the rise in inflation expectations (Michigan 5-Year expectations at 3.2%) suggests the Federal Reserve may face challenges in declaring a complete victory over inflation.

📈 Millionsworth View: Navigating the Global Economic Landscape

How should investors interpret these shifts? The divergence between India’s pro-growth stance and the broader Global Economic Landscape offers specific opportunities for portfolio adjustment.

For Equity Investors: Look at Rate-Sensitives The RBI’s rate cut is a positive trigger for domestic sectors.

- Analysis: Lower interest rates typically reduce the cost of capital for corporations and boost consumer demand for loans.

- Focus Areas: Sectors such as Banking, NBFCs, Real Estate, and Automobiles generally benefit from this cycle. With Fitch upgrading the GDP forecast, domestic cyclical stocks appear well-positioned compared to export-oriented sectors facing global headwinds.

For Debt Investors: Opportunity in Duration The domestic rate cycle has turned, distinct from the global trend.

- Analysis: With the repo rate at 5.25% and inflation projected to remain low, bond yields are likely to soften.

- Strategy: Data suggests this is a favorable environment for medium-to-long duration funds. Investors looking to lock in higher yields may consider acting before the market fully prices in future cuts.

For Commodity Investors: The Role of Hedges

- Analysis: With US inflation rising to 2.8% and the BOJ potentially hiking rates, currency markets (Dollar vs. Yen vs. Rupee) may see increased volatility.

- Strategy: In an uncertain Global Economic Landscape, Gold continues to serve as a portfolio diversifier. It acts as a hedge against potential currency fluctuations arising from the divergence between US, Japanese, and Indian monetary policies.

Conclusion

The week ending December 6, 2025, marks a significant point of separation in the Global Economic Landscape. India’s move to cut rates contrasts sharply with the US battling sticky inflation and Japan preparing to hike rates. For investors, this highlights the importance of asset allocation—balancing the growth potential of the Indian domestic market with the necessary hedges against global monetary shifts.

Disclaimer: This blog is for informational purposes only and does not constitute financial advice. Please consult with a qualified professional before making any investment decisions.