Indian Economy & Regulatory Shifts:

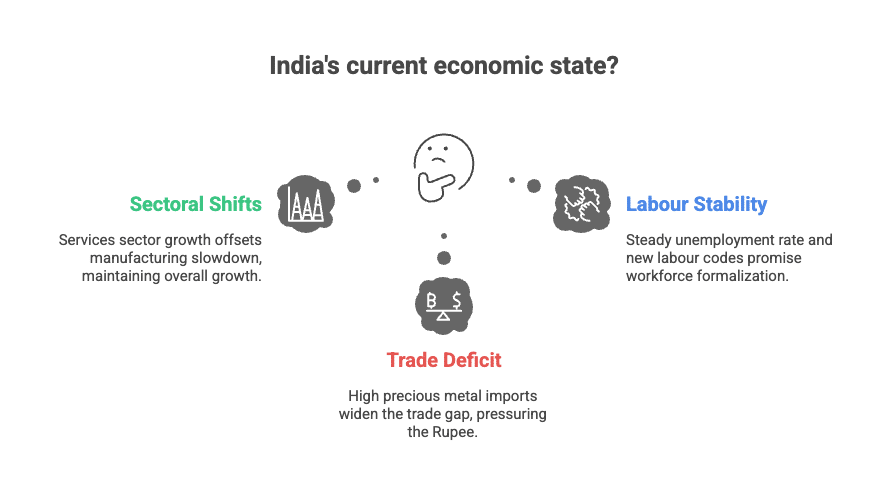

The Indian economy presented a picture of structural resilience this week, even as it grapples with external imbalances. On the activity front, a clear divergence has emerged: while manufacturing momentum cooled slightly, the services sector surged, keeping the overall growth narrative intact. However, macro-stability faces a test from the external sector, where an insatiable domestic appetite for precious metals has widened the trade gap.

- Sectoral Shifts: The HSBC Flash Manufacturing PMI eased to 57.4, while the Services PMI rose to 59.5, indicating that domestic consumption of services is currently the primary growth driver.

- Trade & Currency: The merchandise trade deficit hit a record high of $41.68 billion, driven largely by gold and silver imports. While this has pressured the Rupee, the RBI clarified that the currency’s depreciation is due to global dollar demand rather than domestic weakness.

- Labour Stability: The unemployment rate held steady at 5.2%, and the historic implementation of the four new labour codes this week promises to further formalize the workforce.

On the regulatory front, the focus remained heavily on deepening financial markets and enhancing global connectivity. The Reserve Bank of India took a significant step toward internationalization by agreeing to link domestic payment systems with the European Union, facilitating smoother cross-border flows. Simultaneously, SEBI signalled a major maturing of the markets by announcing a calibrated approach to include REITs and InvITs in indices, a move that will likely channel more passive flows into infrastructure and real estate. While regulators are opening doors for traditional assets, they remain firmly cautious on the alternative front; the RBI reiterated its wariness regarding cryptocurrencies, and SEBI clarified it has no mandate to regulate “digital gold,” leaving investors in those segments without a regulatory safety net.

🇺🇸 United States: The “Soft Landing” Narrative Persists

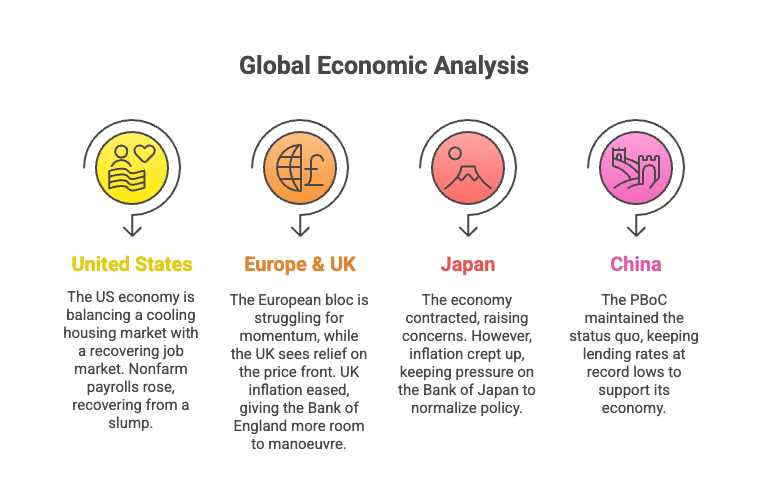

The US economy continues to defy recession fears, balancing a cooling housing market with a recovering job market.

- Labor Market Bounce-back: Nonfarm payrolls rose by 119,000 in September, recovering from a slump in August. However, the unemployment rate ticked up slightly to 4.4%, suggesting the labor market is loosening but not breaking.

- Fed Outlook: Federal Reserve minutes suggest policymakers are leaning toward further rate cuts, though they remain data-dependent.

- Housing: Existing home sales edged up to 4.10 million, showing slight improvement despite the high-interest environment.

🇪🇺 Europe & 🇬🇧 UK: Inflation Cools, Growth Stalls

The European bloc is struggling for momentum, while the UK sees relief on the price front.

- Eurozone Contraction: The Flash Manufacturing PMI slipped to 49.7, indicating a contraction in factory activity.

- UK Price Relief: UK inflation eased to 3.6% (down from 3.8%), giving the Bank of England more room to manoeuvre. However, consumer confidence took a hit, falling to -19.

🇯🇵 Japan & 🇨🇳 China: The Asian Mix

- Japan: The economy contracted by 1.8% (annualized) in Q3, raising concerns. However, inflation crept up to 3.0%, keeping pressure on the Bank of Japan to normalize policy.

- China: The PBoC maintained the status quo, keeping lending rates at record lows to support its economy.

What the Indicators Are Saying to Investors

For Equity Investors: The narrative for equities remains cautiously optimistic, specifically for the Indian markets. The robust services PMI and the implementation of labour codes suggest that the domestic growth engine is functioning well, which is positive for earnings. The regulatory push to include REITs in indices is a specific signal for the Real Estate and Infrastructure sectors, likely leading to better liquidity and valuation discovery. Investors should look at these structural reforms as long-term buy signals, even if short-term volatility persists due to currency fluctuations.

For Debt Investors: The outlook here is nuanced. While the global trend—led by the US and UK—points toward cooling inflation and potential rate cuts, India’s domestic situation is trickier. The record trade deficit and the resulting pressure on the Rupee may prevent the RBI from cutting rates aggressively in the near term to protect the currency. Consequently, debt investors might find safety in the short-to-medium end of the yield curve (such as liquid funds or short-term corporate bonds) rather than betting on immediate long-term yield compression.

For Commodity Investors (Gold & Silver): The indicators are flashing a strong bullish signal for precious metals. The record trade deficit in India was driven primarily by gold and silver imports, proving that physical demand is robust regardless of price. Furthermore, with Japan contracting and the Eurozone struggling, gold retains its “safe haven” premium globally. The sharp jump in the value of India’s forex reserves, attributed to gold revaluation, further underscores the metal’s strength in the current economic climate.

As we navigate a world where domestic growth stories diverge from global headwinds, the ability to distinguish between structural strength and temporary noise becomes the investor’s greatest asset. However, financial landscapes are complex and every portfolio is unique. We strongly encourage you to consult your personal financial advisor and weigh all available facts carefully before making any investment decisions.