This weekly edition of the Global Macro and Market Watch for the period ending September 27, 2025, underscores a prevailing theme of policy assertiveness in India set against a backdrop of mixed, yet generally moderating, global economic activity. Domestically, the government reinforced its commitment to capital expenditure and structural reform, while the Reserve Bank of India (RBI) and SEBI focused on strengthening financial sector stability and digitization. Internationally, the US economy showed continued strength in Q2 GDP figures, but high-frequency data indicated a broad slowdown in manufacturing across the US, Europe, and Asia, suggesting a cautious global environment heading into the final quarter of the calendar year.

🇮🇳 India: Policy Prowess and Domestic Resilience

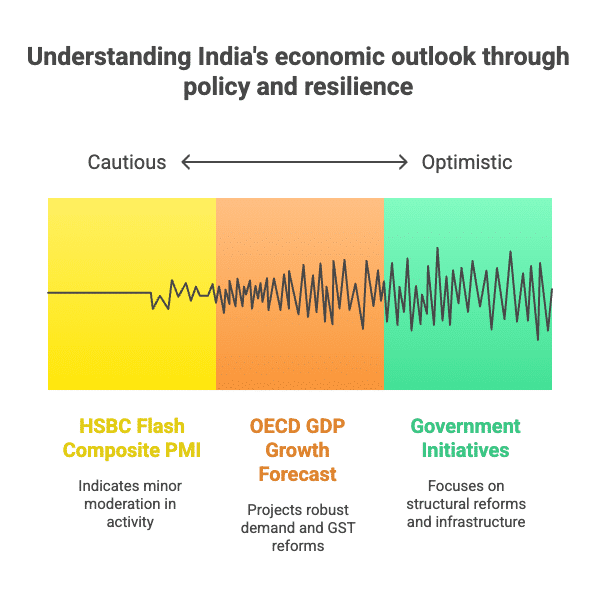

India’s economic data points were largely constructive, anchored by a strong 6.3% expansion in core sector output for August, a sharp acceleration from the previous month. This domestic momentum led the OECD to raise India’s GDP growth forecast for 2025 to 6.7%. Government initiatives were prolific, including the announcement of ₹1 trillioninvestment for port connectivity projects and the launch of a National Shipbuilding Mission. In the regulatory space, the RBI and SEBI strengthened financial security by issuing new directions for digital transactions and raising the minimum net worth for custodians. A deeper dive into the data reveals the continuing resilience and strong fundamentals that shape the Indian segment of our Global Macro and Market Watch.

For investors, the strong domestic narrative—driven by accelerating core infrastructure activity and large-scale government capital expenditure plans—remains the key takeaway. The policy signals favour sectors tied to national infrastructure (roads, ports, railways), manufacturing (given policy support like the shipbuilding mission), and the financial sector, which benefits from RBI’s efforts to deepen and secure market participation. While the slight softening of the PMI suggests some near-term cyclical pressures, the long-term case for Indian equities, particularly in growth-enabling sectors, is reinforced by the government’s sustained focus on structural reforms. In fixed income, the commitment to fiscal targets is positive, but the strong domestic growth and core sector rebound necessitate a cautious, short-duration strategy.

🇺🇸 United States: Economic Strength and Manufacturing Moderation

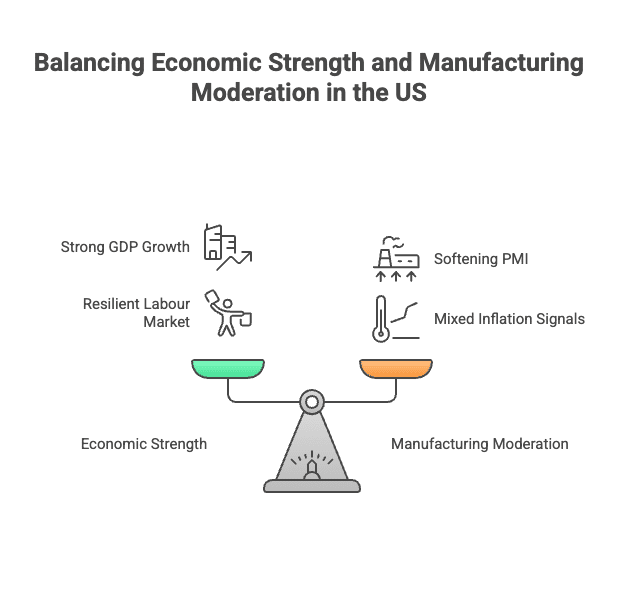

The US economy delivered a strong underlying performance, with Q2 2025 GDP expanding at an annualized rate of 3.8%, a substantial increase from the revised Q1 figure. Labour market health was also confirmed as Initial Jobless Claims declined to 218,000 in September. However, a divergence appeared in high-frequency sentiment data: the S&P Global Flash Manufacturing PMI eased to 52 in September, while the S&P Global Flash Composite PMI fell to 53.6, suggesting a loss of momentum in the industrial sector. Inflation signals were mixed, with the overall PCE Price Index rising 2.7% year-over-year in August, yet the annualized Q2 PCE Price trend slowed to 2.1%. The housing market also exhibited complexity, with Existing Home Sales easing, while new home sales jumped by 20.5% in August, alongside a slight drop in building permits.

The strong Q2 GDP and resilient labour market reinforce the ‘soft landing’ narrative and support equity sectors tied to consumer discretionary spending. However, the softening manufacturing PMI, combined with the mixed inflation signals, suggests that the Federal Reserve will likely maintain its data-dependent approach. Investors should favour quality equities, particularly those in the services and technology sectors, which are less exposed to the industrial slowdown. In fixed income, the conflicting inflation data (rising YoY PCE vs. slowing QoQ PCE) keeps intermediate Treasuries attractive for those betting on continued price moderation, while the overall economic resilience limits the probability of aggressive rate cuts.

🇪🇺 Eurozone & 🇬🇧 UK: Mixed Signals in Europe

European data confirmed a broad-based weakness in the industrial sector. The Eurozone’s HCOB Flash Manufacturing PMI fell back into contraction at 49.5 in September, but this was partially offset by a resilient services sector, where the PMI climbed to 51.4, resulting in the Composite PMI holding steady at 51.2. Consumer confidence in the Eurozone, however, eased to -14.9. Similarly, in the United Kingdom, both the S&P Global Flash Manufacturing PMI (46.2) and the Services PMI (51.9) declined, causing the Composite PMI to slip to 51.0, indicating a synchronized slowdown in overall private sector growth.

The European picture favours defensive and services-oriented equity exposures, as manufacturing activity contracts in both the Eurozone and the UK. The stability of the Composite PMI in the Eurozone, supported by services, suggests domestic demand is still preventing a sharp downturn. Investors should avoid cyclical industrial exposures in Europe and instead look towards high-quality domestic service providers and financials. For fixed income, the slowing growth momentum supports sovereign bond prices, although the mixed data suggests central banks are likely to remain on hold for the near term; investors should prioritize quality and avoid taking on excessive duration risk.

🇯🇵 Japan & 🇨🇳 China: Policy Stability

In Asia, Japan’s S&P Global flash Manufacturing PMI eased to 48.4 in September, pushing the Composite PMI to 51.1, highlighting continued softness in the industrial sector despite a more resilient services component. In China, the People’s Bank of China (PBOC) maintained its focus on monetary stability by holding the one-year Loan Prime Rate (LPR) at 3.0% and the five-year LPR at 3.5% for the fourth consecutive month, signalling that policy easing efforts have been temporarily paused as the central bank monitors the effect of previous stimulus measures.

The data suggests a continued divergence in Asian growth drivers, with Japan’s industrial engine struggling while China prioritizes policy stability over immediate, aggressive stimulus. For equity investors, Japan’s market is likely to favour domestic consumption-oriented stocks over exporters. In China, the stable LPRs signal that credit conditions will remain supportive but do not indicate new, large-scale stimulus, warranting a selective approach focused on structural themes like technology, renewables, and policy-supported infrastructure. In fixed income, the policy stability in both countries suggests avoiding long-duration bets, with preference given to quality issuers.

🧭 Cross-Market Strategy Snapshot

| Region | Equity View (Sectors) | Fixed Income View (Bonds) |

| 🇮🇳 India | Infrastructure, Financials (BFSI), Affordable Housing(Policy support), Renewables (ALMM/PLI focus). | Short-duration debt (Amid strong core sector growth and inflation watch). |

| 🇺🇸 US | Consumer Discretionary, Services, Housing-linked(Strong Q2 GDP, declining jobless claims). | Intermediate Treasuries (Growth strong, but inflation signals are mixed). |

| 🇪🇺 Eurozone | Services, Domestic Industrials (Services resilience offsets manufacturing contraction). | Quality Euro debt (Modest growth, avoiding excess duration). |

| 🇬🇧 UK | Defensive equities, Services (As overall Composite PMI momentum slips). | Short-duration Gilts (Slowing growth momentum). |

| 🇯🇵 Japan | Domestic Consumption, Defensive Sectors(Manufacturing weakness continues). | Short-duration JGBs. |

| 🇨🇳 China | Policy-supported sectors (Infra, Green Tech) (LPR stability maintained). | Quality issuers, avoiding long duration. |

✍️ Millionsworth Takeaway

This week underscored the theme of diverging global dynamics. India continues to distinguish itself with robust domestic policy momentum, characterized by large-scale capital expenditure and targeted regulatory reforms designed for stability and growth. While global manufacturing faces a mild, synchronized slowdown, the resilience of the US economy (Q2 GDP) and European services sectors provides important counterbalances. For investors, the path forward demands selectivity: focus on domestic policy beneficiaries in India—especially infrastructure and housing—while maintaining a duration-aware and quality-focused approach in global fixed income markets as growth and inflation signals vary across regions. We will continue to track these trends in our next Global Macro and Market Watch update.